What the scheme is

Sri Lanka’s Public Service Pension Scheme (PSPS) covers permanent central-government employees who complete the qualifying service and retire under the stipulated rules. It is defined-benefit and pay-as-you-go: benefits are set by regulation and paid from current revenues rather than from an invested fund. Separate regulations govern teachers, police, and the armed forces, but the fiscal logic is the same.

Two important adjuncts sit alongside the core pension:

1. W&OP (Widows/Widowers & Orphans’ Pension): a contributory survivor-benefit deduction from the employee’s salary that provides benefits to eligible dependants after the pensioner’s death.

2. Gratuity: a lump-sum payment at retirement, calculated against service and salary rules.

Private-sector workers are not in PSPS; they primarily build retirement savings through EPF/ETF or approved funds, which are defined-contribution arrangements.

A short history

- Early colonial period (19th century): pensions for civil officers were introduced to secure a professional service. Survivor benefits were formalised under Widows’ & Orphans’ provisions.

- 1900s–1950s: mandatory civil-service pension rules took firmer shape as the bureaucracy expanded.

- Post-independence: the scheme broadened with the growth of education, health, and administration. Separate survivor coverage for female officers was later legislated to ensure parity.

- Devolution era: provincial services obtained their own pension statutes, but liabilities still flow from public budgets.

- 1990s–today: periodic amendments refined eligibility ages, qualifying service, commutation limits, re-employment rules, and indexation practices. Budget documents increasingly highlighted pension outlays as a rising share of current expenditure.

The underlying model has stayed constant: a state promise financed out of taxes, with benefits linked to service length and terminal pay.

How benefits typically accrue

Exact formulas are set by statute and circulars. In practice, three levers shape the eventual pension:

- Service years: longer service increases the accrual factor toward a capped replacement rate.

- Pensionable pay: usually the final or averaged basic salary plus pensionable allowances as defined in circulars.

- Retirement channel: normal retirement, medical invalidity, or compulsory retirement follow different rules on age and qualifying service.

W&OP runs on contributions during service and pays survivors according to marital and dependent status rules. Gratuity is paid at exit under a separate formula and does not affect the monthly pension once paid.

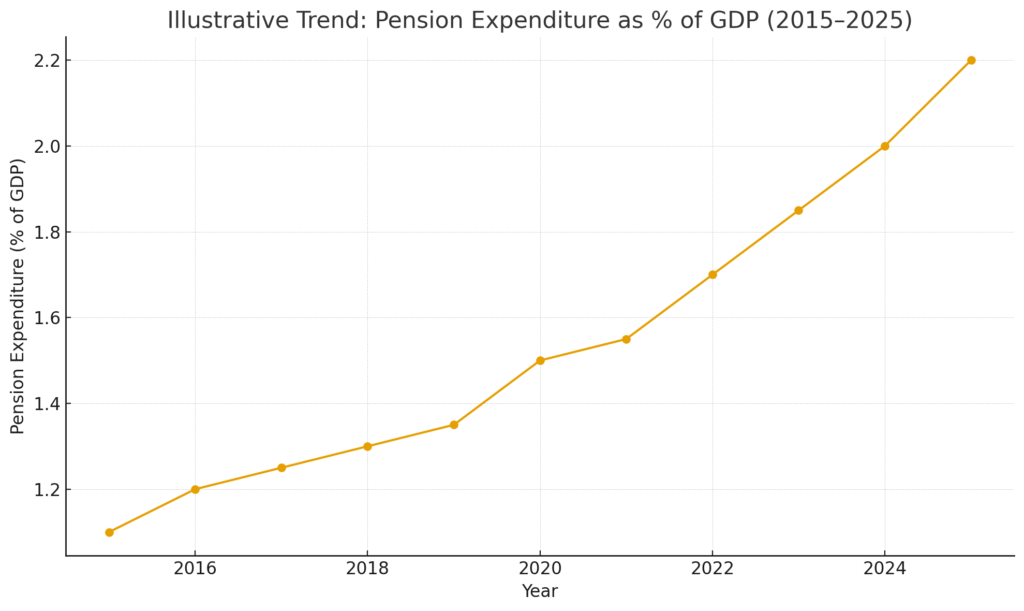

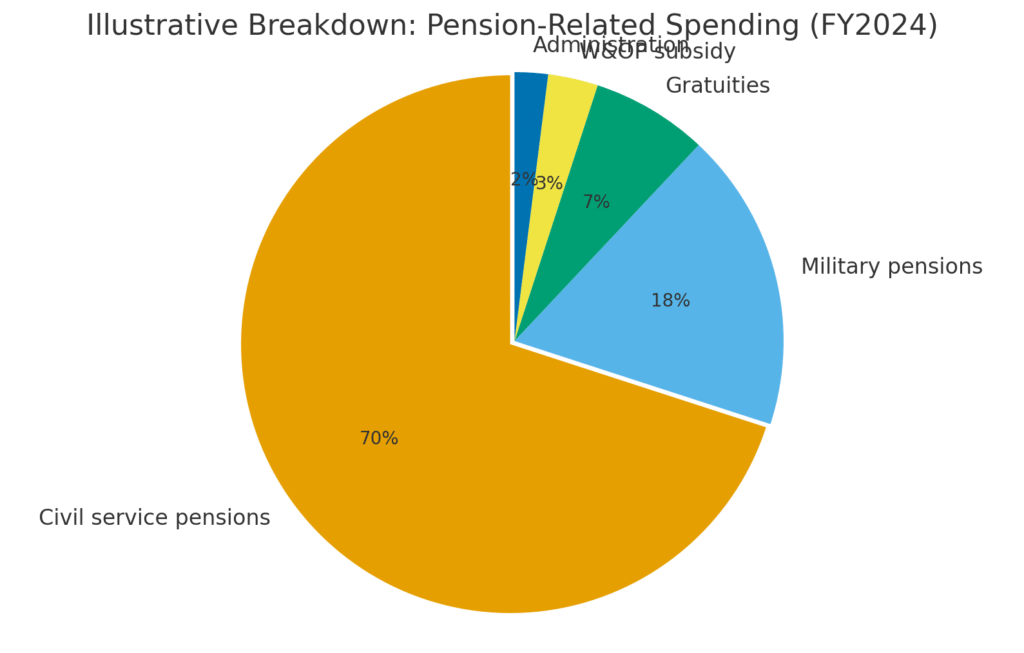

The numbers at a glance

The following visuals are illustrative to show trends and composition for communication. Replace with official figures when publishing a policy brief.

- Figure 1 shows a steady rise in pension outlays relative to GDP, reflecting demographic ageing, earlier hiring bulges reaching retirement, and salary revisions feeding through to pension bases.

- Figure 2 depicts a typical composition: the civil service pension dominates; military pensions are material; gratuities and W&OP subsidies are smaller but non-trivial.

Why costs rise

- Demographics: Longer life expectancy raises years in payment.

- Pay revisions: Upward adjustments to scales flow into pensionable pay.

- Maturity: As larger cohorts reach retirement, cash needs climb.

- Design choice: A non-contributory, pay-as-you-go design concentrates risk on the budget rather than on a fund.

Equity questions

- Public vs private: Public servants receive a guaranteed lifetime benefit; private workers rely on accumulated balances and investment returns.

- Intra-public equity: Different services may have different retirement ages and generous early-retirement pathways, affecting horizontal fairness.

- Gender and survivors: W&OP improved coverage for dependants, but contribution rates and eligibility rules must be kept aligned with modern family structures.

What reform looks like

Policymakers worldwide tend to use parametric tools first, because they preserve the social contract while controlling costs:

- Adjust retirement age to reflect longevity.

- Refine accrual factors or caps to align replacement rates with affordability.

- Harmonise pensionable pay definitions to reduce spikes from last-minute allowances.

- Indexation rules that balance inflation protection with fiscal space.

- Contribution tweaks for survivor schemes so that benefits are self-financing.

- Data and audit discipline: accurate pension rolls, digital life certificates, and transparent reporting on new awards, deaths, and suspensions.

Structural options exist but are harder to implement:

- Notional defined-contribution (NDC) tiers for new entrants while preserving accrued rights.

- Dedicated funding windows (e.g., a modest pre-fund with strict governance) to smooth shocks, not to fully fund promises.

- Convergence of rules across services over time to reduce arbitrage.

Practical guidance for stakeholders

- HR and line ministries: keep digital service records complete and standardised from day one. Missing months and ad-hoc allowances create disputes and delays at retirement.

- Unions: focus on clarity of rules and predictable indexation rather than one-off discretionary increases that generate future volatility.

- Budget officers: publish an annual pension dashboard covering new retirees, average pension, indexation cost, and survivor caseload.

- Researchers and media: distinguish between core pensions, gratuities, and W&OP; do not mix these lines when quoting totals.

FAQ

- Is the pension guaranteed by a fund? – No. It is paid from the budget each year subject to appropriation. That is the essence of pay-as-you-go.

- Does the private sector get the same deal? – No. Private workers rely on EPF/ETF balances and investment returns, not a government DB pension.

- Will reforms cut current pensioners’ payments? – Standard practice is that changes are prospective. Accrued rights are protected; parameters change for future service or new entrants.