Introduction: A New Front in the U.S.–China Trade War

A new 110% tariff on Chinese imports imposed by Donald Trump has sent shockwaves through global markets(China Tariffs). This sweeping move – effectively doubling the cost of goods from China – marks an unprecedented escalation in the ongoing U.S.–China trade war. Announced as part of Trump’s pledge to pursue “reciprocal tariffs,” the policy aims to pressure Beijing by making Chinese products prohibitively expensive in the U.S. The implications extend far beyond Washington and Beijing. Asia’s economy stands on the front lines of this upheaval, and countries like Sri Lanka are closely watching how these Trump tariffs will ripple through trade, investment, and geopolitical dynamics. In this analysis, we examine the broader China trade war context, compare these tariffs with previous rounds under Trump and Biden, and assess the Asia economy impact – with a special focus on Sri Lanka’s exports, investments, and strategic alignment.

Trump’s 110% Tariffs: What Happened and Why?

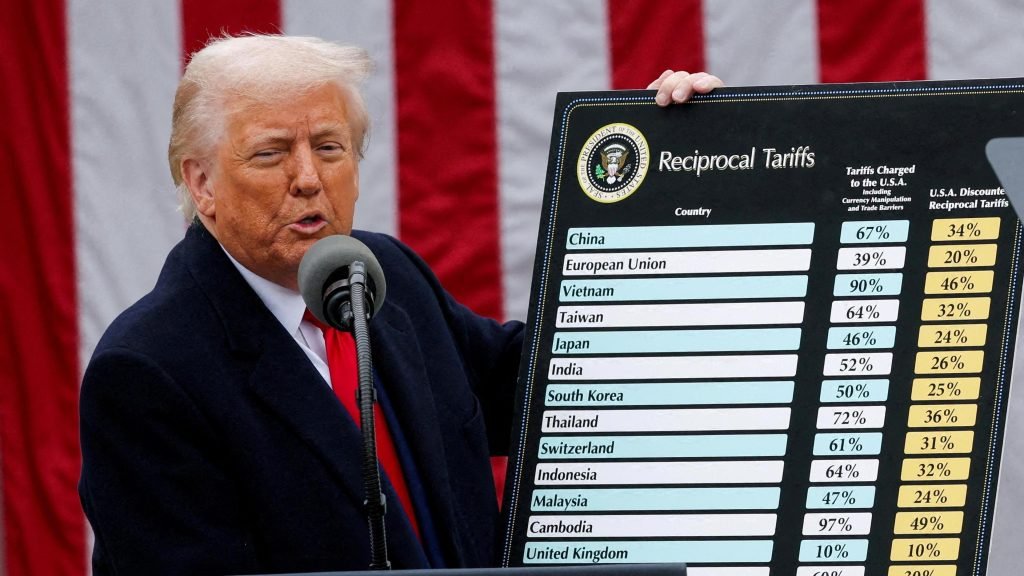

Trump’s latest tariff salvo raises duties on all Chinese imports to over 100% – in effect, more than doubling their price in the U.S. This staggering rate (widely described as a 110% tariff) is the highest U.S. tariff level in living memory, pushing protectionism to heights not seen since the 1930s. The White House rolled out these measures on April 2, a day Trump dubbed “Liberation Day,” invoking emergency economic powers to justify the tariffs as a defense against “unfair” trade practices. Trump argues that foreign nations’ high tariffs and trade barriers have long put American industry at a disadvantage. By slapping “reciprocal” tariffs of equal or greater magnitude, he claims the U.S. is leveling the playing field. For example, officials pointed to other countries’ steep duties (like India’s 100% tariff on certain U.S. goods) to rationalize the across-the-board 10% baseline tariff and much higher country-specific rates. China, with whom the U.S. runs its largest trade deficit, was hit the hardest, now facing what is essentially a tariff wall. The Trump administration’s justification centers on economic nationalism – protecting domestic manufacturers and addressing the trade deficit – even if it means severing supply chains and enduring short-term pain. Critics, however, note that tariffs are ultimately paid by U.S. consumers and businesses through higher prices, and many economists warn this drastic step could backfire.

China’s foreign ministry has condemned the new tariffs as “unilateralism, protectionism and economic bullying”, signaling Beijing’s outrage at the U.S. move. In response, China retaliated with its own hikes (reportedly raising tariffs on U.S. goods to 34%) and vowed further countermeasures. The war of words has been fierce: Beijing denounced Washington’s actions as a threat to international trade fairness, while the Trump administration insisted it would not back down unless China capitulates. This exchange highlights a deepening rift between the world’s two largest economies, stoking fears that the trade dispute could spiral into a broader economic conflict. Companies reliant on U.S.–China commerce are bracing for disruption. Even everyday products like smartphones are caught in the fray – Trump officials claimed Americans can make iPhones domestically, but industry experts caution that abruptly reshoring such complex supply chains is impractical. With each side digging in, the stage is set for a prolonged standoff.

Comparing Past Trade Wars: Trump’s First Term vs. Biden’s Approach

This isn’t the first tariff battle between the U.S. and China. Trump’s first term (2018–2019) saw a series of tariff rounds that kicked off the modern “China trade war.” Back then, tariffs topped out at about 25% on roughly $250 billion worth of Chinese imports, with additional goods taxed at 7.5% after a 2020 Phase One deal. Beijing answered in kind with its own duties on U.S. exports, though the scale was more limited. Those earlier tariffs mainly targeted industrial and intermediate goods at first, sparing many consumer products. The economic pain was noticeable but not catastrophic – supply chains shifted to countries like Vietnam for certain products, and the two sides eventually struck a partial truce. Notably, Sri Lanka and other Asian exporters saw some indirect benefits during that period as U.S. importers sought alternatives to Chinese suppliers, boosting orders from elsewhere in Asia.

Under President Joe Biden, the trade war tone shifted but did not fully disappear. Biden opted to maintain most Trump-era tariffs on China rather than remove them overnight. However, he refrained from new tariff escalations and instead focused on targeted measures (for example, export controls on Chinese high-tech imports and cooperating with allies on trade issues). Biden’s strategy was more about managed competition with China – keeping pressure but also avoiding further tit-for-tat tariff hikes that could hurt U.S. consumers amid pandemic recovery. The result was a tense but stable status quo through 2021–2024, with tariffs averaging around 19% on Chinese goods and ongoing negotiations behind the scenes. This relative calm has now been upended by Trump’s return to aggressive tariffs. Today’s 110% tariff far overshoots anything implemented in the 2010s, reflecting a more hardline stance. Compared to prior rounds, the current measures are broader (covering virtually all imports) and much steeper in rate. The contrast is stark: where Biden sought targeted decoupling and alliance-building, Trump has opted for an all-out tariff offensive. This historical context underscores just how extraordinary the new tariff policy is – it represents the culmination of years of trade tensions, taken to an extreme.

Asia’s Economic Fallout and Global Ripple Effects

The impact on Asia’s economy from these tariffs could be profound and multifaceted. China’s role as the region’s economic engine means that shocks to China will reverberate across Asia. A 110% tariff effectively prices Chinese goods out of the U.S. market, which could reduce China’s export earnings and industrial output dramatically. Slower Chinese growth or factory shutdowns would hurt Asian countries that supply components and raw materials to China. For instance, exporters of electronics parts in Taiwan, South Korea, and Malaysia may see orders drop if Chinese assembly plants cut production. Likewise, commodity suppliers – from Australian miners to Southeast Asian rubber producers – could feel the pinch as Chinese demand ebbs. The Asia economy impact is not all negative, however. Some manufacturing could be diverted to other Asian countries: U.S. importers might turn to Vietnam, Bangladesh, or India to source products no longer competitively available from China. Indeed, during the 2018–19 trade war, Vietnam’s exports to the U.S. jumped as firms shifted supply chains. We may see a similar boost for certain ASEAN economies if they are not subject to equivalent U.S. tariffs. (It’s worth noting, though, that Trump’s new policy imposes a base 10% tariff on all countries, and higher rates on many others with trade surpluses. So the advantage for alternate Asian suppliers might be limited if they too face at least some tariffs.)

Broader global economic effects are already emerging. Financial markets reacted nervously to Trump’s tariff announcement – the news triggered an immediate stock market sell-off amid fears of rising costs and eroding corporate profits. Major U.S. indices fell as investors grappled with the possibility of higher inflation and slower growth. Banks and analysts are warning of recession risks: Goldman Sachs quickly raised the probability of a U.S. recession, citing “larger tariffs, greater policy uncertainty, [and] declining business and consumer confidence”. They project U.S. GDP growth could fall sharply in 2025, potentially to near-zero, if the full tariff regime remains. A U.S. slowdown combined with a China slowdown is bad news for the global economy. The OECD and IMF have downgraded growth forecasts, seeing Trump’s tariffs as a new drag on world trade. Consumers worldwide may feel the effects through higher prices on goods – from electronics to apparel – as supply chains adjust and production costs rise. At the same time, inflationary pressures could force central banks to hike interest rates more, further damping growth. In short, the tariff escalation adds another layer of uncertainty to a world economy already dealing with post-pandemic recovery and geopolitical tensions. Asia, being heavily trade-dependent, finds itself walking a tightrope: some countries might gain short-term export windfalls as trade shifts, but the overall risk is a net negative if a full-blown trade war stalls global demand.

Sri Lanka’s Stakes: Trade, Investment, and Geopolitical Alignment

Sri Lanka, as a small open economy in Asia, is particularly vulnerable to the fallout from a U.S.–China trade war. The United States is one of Sri Lanka’s biggest export markets, while China is its largest source of imports and a key investor. Here’s how Trump’s tariff escalation may affect Sri Lanka’s trade, investment, and geopolitical alignment:

- Trade and Sri Lanka’s Exports: Sri Lanka’s export sector – especially apparel – relies heavily on U.S. consumers. About 23% of Sri Lanka’s exports (and nearly 40% of its garment exports) go to the U.S. Any U.S. economic slowdown or drop in consumer spending due to tariff-induced price hikes could hurt demand for Sri Lankan goods. Moreover, Trump’s tariff strategy isn’t only singling out China; it includes across-the-board duties that have hit many countries. Reports indicate Sri Lankan products might even face new U.S. tariffs (one analysis noted a 44% U.S. tariff on Sri Lankan goods under the “reciprocal” scheme). Such barriers would make Sri Lanka’s garments and tea less competitive, squeezing an economy already recovering from crisis. On the import side, Sri Lanka buys a huge volume of goods from China – over $4.3 billion worth in 2024, ranging from machinery to consumer products. If Chinese firms cut production or redirect trade due to U.S. tariffs, Sri Lanka could face supply disruptions or higher import prices. Conversely, a glut of Chinese goods looking for alternative markets could lead to cheaper imports for countries like Sri Lanka (for example, electronics or steel), which might slightly ease local inflation. Overall, the impact on Sri Lanka’s exports is a major concern: reduced access to U.S. markets or weaker global demand directly threatens Sri Lanka’s foreign earnings and jobs in export industries.

- Investment and Economic Aid: China has been a major investor and lender in Sri Lanka for the past decade, funding infrastructure projects like ports, highways, and power plants. If China’s economy slows significantly under the weight of tariffs, Beijing might scale back its foreign investments or become more cautious in lending. This could jeopardize planned projects in Sri Lanka or delay much-needed investment inflows. On the other hand, China may also double down on initiatives like the Belt and Road in friendly countries to shore up political alliances when facing U.S. pressure. Sri Lanka might thus see offers of continued support from China – but potentially at the cost of incurring more debt. Meanwhile, the United States and its allies (India, Japan) could attempt to counterbalance Chinese influence by ramping up their own engagement with Sri Lanka. For instance, there have been talks of U.S. and Indian investments in Sri Lankan ports and renewable energy, partly to provide alternatives to Chinese-funded projects. Trump’s aggressive stance on China might come with carrots for countries that distance themselves from Beijing. However, if Sri Lanka is perceived as too close to China, it might also risk being caught in any broader U.S. punitive measures (such as loss of trade preferences). The island’s economic recovery from its recent debt crisis hinges on attracting diversified foreign investment – a volatile global trade climate makes that more challenging.

- Geopolitical Alignment: The intensifying U.S.–China rift forces smaller countries into a delicate balancing act. Sri Lanka has traditionally tried to maintain a neutral stance, benefiting from strong ties with China (for investment) while also keeping the U.S. and India onside. A full-blown trade war raises the stakes of this balance. Sri Lanka may come under subtle pressure to align more clearly with one camp or the other. The U.S. might push Sri Lanka to support its vision of a “free and open Indo-Pacific,” implicitly asking for caution in dealings with China. China, conversely, will expect continued friendship and could offer economic sweeteners to ensure Sri Lanka doesn’t side with Western critiques. We could see geopolitical recalibrations such as Sri Lanka seeking closer economic integration with regional initiatives led by China (like the Regional Comprehensive Economic Partnership, in which China is a member) to hedge against losses from Western markets. Alternatively, Sri Lanka might pursue new trade agreements with other partners to reduce reliance on any single country. There is also a strategic element: Sri Lanka’s location in the Indian Ocean makes it important in China’s maritime Belt and Road strategy and in the U.S.’s regional plans. As the U.S.–China trade war spills into a broader strategic rivalry, Colombo’s foreign policy decisions will be scrutinized. The government will likely strive to avoid taking sides openly – for example, by continuing to welcome Chinese investment while also engaging with U.S. initiatives – but this neutrality could be tested if the economic situation deteriorates. In summary, the tariff conflict adds another layer of complexity to Sri Lanka’s foreign relations, potentially affecting everything from port deals to defense cooperation, and will require adept diplomacy to navigate.

Conclusion: Navigating an Uncertain Trade Landscape

The 110% tariff on Chinese imports unleashed by President Trump represents a dramatic turning point in the U.S.–China economic confrontation. Its ripple effects are spreading across Asia and the globe, disrupting trade flows and challenging policymakers to respond. For Asia, the move injects uncertainty into a regional economy that has long been intertwined with China’s rise. Countries may find opportunities in the shake-up – an order diverted here, a factory relocated there – but they also face the broader headwinds of a trade war that could dampen growth across the board. Sri Lanka’s situation exemplifies the delicate balance emerging economies must strike. The island nation’s prosperity is tightly linked to external markets and great-power partners: it depends on open access to U.S. consumers, affordable imports and loans from China, and a peaceful environment to foster investment. A prolonged Trump tariffs regime threatens to upset this balance, presenting Sri Lanka with both economic pitfalls and diplomatic dilemmas.

In crafting its response, Sri Lanka (and others in Asia) will need to emphasize resilience and diversification. That means exploring new export markets, improving competitiveness to absorb higher tariffs if needed, and managing debt wisely if external financing conditions change. Diplomatically, staying neutral yet pragmatic will be key – maintaining good relations with China for development needs, while engaging with the U.S. and regional powers to ensure one is not overly reliant on any single partner. The global trading system itself is at a crossroads. If the China trade war continues to escalate, we may see a fundamental realignment of supply chains and trade alliances in the coming years. On the other hand, there remains the possibility of negotiation and de-escalation, if cooler heads recognize the mutual damage being done. For now, Asia and Sri Lanka can only brace for volatility. Trump’s tariffs have raised the stakes considerably, and the world will be watching closely to see whether this bold gamble will reset trade relationships – or simply set off a chain reaction of economic pain. In these uncertain times, one thing is clear: the decisions made in Washington and Beijing in the months ahead will have far-reaching consequences for the Asia economy and beyond, shaping the trajectory of globalization and growth in the years to come.