In a significant development for Sri Lankan taxpayers, the Cabinet of Ministers has approved changes to the personal income tax (PIT) system following negotiations with the International Monetary Fund (IMF). This new tax structure, set to take effect on April 1, 2025, aims to offer relief to middle-income earners while maintaining fiscal discipline. Here’s a detailed breakdown of what the new tax changes entail and their potential impact.

Overview of the New Tax Structure

The new personal income tax structure approved by the Cabinet introduces several key changes:

- Tax-Free Threshold: The tax-free threshold remains unchanged at Rs. 1.2 million per year. This means that income up to this amount will not be subject to income tax.

- Tax Bands: The range of tax bands will be adjusted. Previously, the tax bands were set at Rs. 500,000. Under the new structure, this will increase to Rs. 720,000. This change aims to provide some relief to those in the lower and middle-income brackets by reducing the number of individuals who fall into higher tax bands.

- Marginal Tax Rates: The marginal tax rates will remain the same. The rate of 6% will apply within each band, and the top marginal tax rate will continue at 36%. This structure ensures that while some relief is provided through adjusted tax bands, high-income earners will continue to contribute significantly.

Why These Changes Were Necessary

The Finance Ministry has emphasized that these adjustments are designed to address public concerns about the tax burden, particularly for middle-income earners. The previous tax structure, implemented in January 2023, significantly increased the tax burden due to a steep rise in tax bands and rates. This was a necessary measure in response to the severe economic crisis Sri Lanka faced at that time.

The goal of the new tax structure is to balance relief for taxpayers while still meeting fiscal targets set under the IMF Extended Fund Facility (EFF) program. The EFF program is part of Sri Lanka’s broader strategy to stabilize its economy and restore financial health. Achieving a primary budget surplus of 2.3% of GDP by the end of 2025 is a key target of this program, which also requires increasing government tax revenue to 14% of GDP.

Impact on Different Income Groups

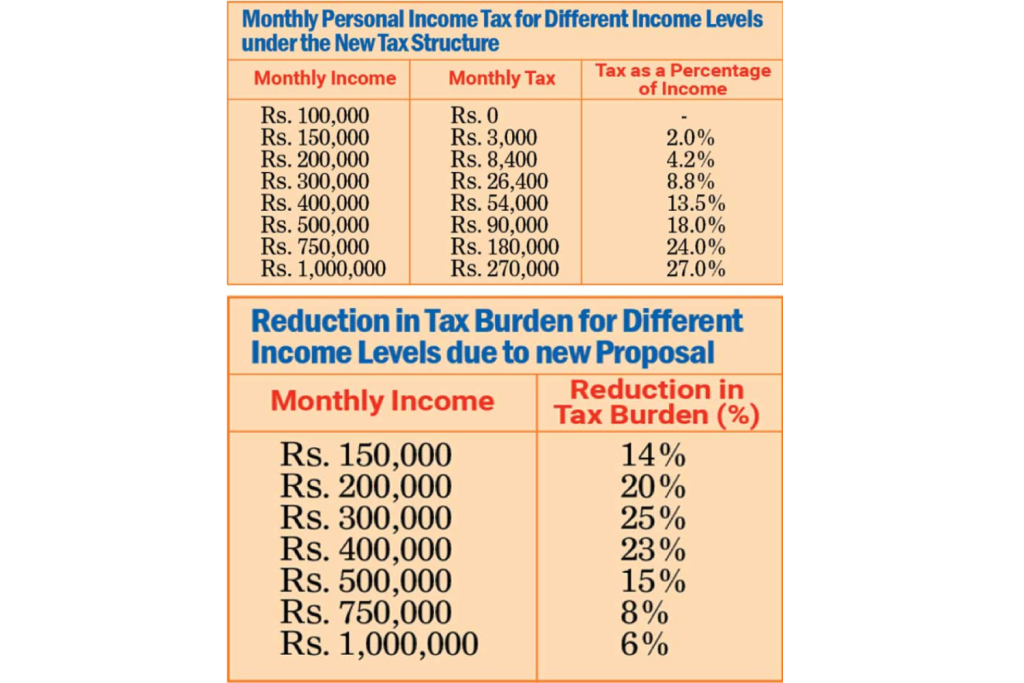

The new tax structure aims to provide targeted relief, primarily benefiting middle-income earners. For instance, consider a person earning Rs. 130,000 per month. Under the current structure, this individual pays Rs. 1,800 per month in taxes, which is approximately 1.4% of their total income. By increasing the tax bands, the new structure aims to reduce the tax burden for individuals in similar income brackets.

However, the tax-free threshold remains at Rs. 1.2 million. Increasing this threshold could potentially reduce the tax base significantly and impact overall revenue. Therefore, maintaining the current threshold helps ensure that the government can still generate necessary revenue to support its fiscal objectives.

High-income earners, who can afford to contribute more in taxes, will see limited relief. This approach aligns with the principle that those with higher financial capacity should bear a larger share of the tax burden.

Revenue Implications and Fiscal Discipline

The Finance Ministry projects that the revenue impact of the new tax structure will be approximately 0.07% of GDP. To compensate for this revenue reduction, the government has planned additional revenue measures, including increased income from vehicle imports starting in 2025. These measures are intended to offset the revenue loss while supporting fiscal stability.

The government has worked closely with the IMF to ensure that these tax changes do not undermine the broader fiscal targets of the EFF program. Maintaining a balance between providing taxpayer relief and achieving fiscal targets is crucial for restoring and sustaining economic stability.

Historical Context and Reforms

The introduction of significant tax reforms in mid-2022 was a key component of Sri Lanka’s strategy to address the unprecedented economic crisis. The original reforms, which took effect on January 1, 2023, included a tax-free threshold of Rs. 1.2 million and tax bands set at Rs. 500,000 each, with a marginal rate of 6% up to a maximum of 36%.

These reforms were essential due to the depth of the economic crisis and the urgent need for revenue enhancement. The sharp increase in tax impact led to significant public demand for relief, particularly among middle-income taxpayers.

In response, the government initiated discussions with the IMF in September 2023 to seek some relief. However, at that time, revenue targets had not yet been fully met, and making changes to the tax structure less than a year after implementation could have undermined the credibility of the government’s fiscal measures.

By mid-2024, the government had made significant progress in meeting revenue targets and had even exceeded several fiscal targets, including the primary balance target. This improvement allowed for renewed negotiations on the PIT structure during the IMF Staff visit in July 2024.

Looking Ahead

The new personal income tax structure reflects a thoughtful approach to balancing taxpayer relief with the need to maintain fiscal discipline. By adjusting tax bands and maintaining existing thresholds and rates, the government aims to provide meaningful relief to middle-income earners while continuing to meet its fiscal commitments.

These changes are a crucial step in Sri Lanka’s ongoing efforts to stabilize its economy and restore financial health. As the new tax structure takes effect in April 2025, it will be important for both taxpayers and policymakers to closely monitor its impact and adjust as necessary to ensure continued progress toward economic recovery and stability.