Sri Lanka has crossed the hardest miles of debt restructuring. Eurobonds were exchanged in December 2024. Bilateral deals have advanced with Japan, India, and others. According to IMF Mission Chief Evan Papageorgiou, only about US$500 million of the US$28 billion “under the perimeter” remains to be finalised. That is real progress. It is not, by itself, a solution.

This piece explains why the IMF is right to insist that stabilising the flow—the annual budget balance and cash management matters as much as fixing the stock. It also sets out what to watch in the 2026 Budget, where risks sit, and the practical levers that turn a paper adjustment into lasting solvency.

Debt sustainability is a flow problem with a stock constraint

Restructuring reduces the present value of obligations and eases near-term cash crunches. It does not change the mechanics that created the gap between spending and revenue. If primary balances turn negative again, the stock will simply rebuild.

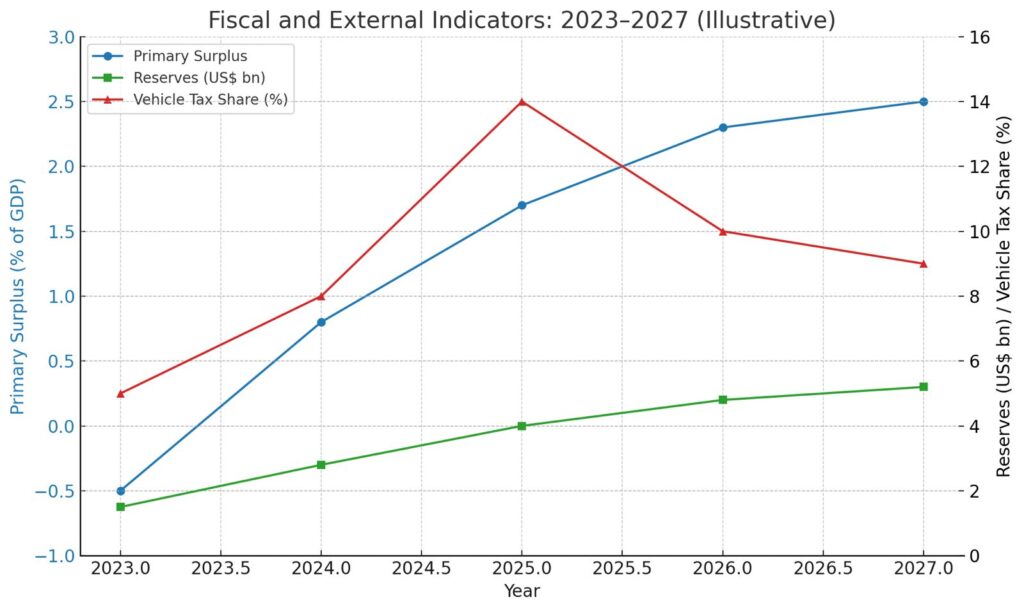

The IMF’s minimum primary surplus target of 2.3% of GDP in 2026 is the fulcrum. Hitting it once is necessary. Sustaining it for several years is what anchors the debt ratio on a downward path while growth recovers and interest costs normalise. That is why the Fund is not only auditing totals but also the quality of spending and revenue inside the Budget. Composition, not just size, determines whether surpluses are politically and economically durable.

Revenue: temporary buoyancy versus structural lift

The standout story this year is the surge in motor vehicle imports and associated taxes. This is a useful, visible sign of demand normalisation and better confidence. It is also, by nature, cyclical and potentially front-loaded after a long import suspension. Relying on it to carry the 2026 revenue baseline is risky.

Policy implication:

- Treat auto-related receipts as one-off windfalls in forecasting.

- Build the Budget on broad-base, persistent sources: VAT base and compliance, PAYE and corporate enforcement, excises with predictable indexation, and estate/property-type instruments where administratively feasible.

- Continue digitalisation of tax administration to reduce leakages and widen the filing net rather than continually raising headline rates on a narrow base.

In short, protect the primary surplus by insulating it from the volatility of single categories like vehicles.

Expenditure: credibility lives in the details

The Fund will judge not just how much the Government spends but what on and how. Three tests matter:

- Targeted social protection. Inflation has retreated, but real incomes for lower-income households remain fragile. Programmes that are targeted, digitised, and time-bounded protect political legitimacy of consolidation at low fiscal cost per beneficiary.

- Growth-positive capex. Port, logistics, grid, and water investments that unlock private activity support the denominator of the debt ratio. The right capital mix improves future revenue without bloating recurrent costs.

- Recurrent discipline. Wage drift, subsidies without automatic pricing rules, and ad hoc transfers erode surpluses quietly. Anchors such as automatic fuel and electricity pricing and medium-term pay frameworks keep the line taut.

SOEs: the hidden deficit

IMF language on “stronger incentives for management” and the new SOE Act signals a push from compliance to performance. The system risk is not a single shock; it is cumulative quasi-fiscal losses that migrate onto the Treasury balance sheet.

What to look for:

- Hard budget constraints. No arrears accumulation between SOEs and the Treasury or between SOEs themselves.

- Commercially enforceable KPIs. Boards must own cash-flow targets and loss-reduction plans, with consequences.

- Transaction programme clarity. Where strategic partnerships, listings, or concessions are planned, put them on a transparent timetable to avoid reform fatigue.

Each percentage point of GDP saved in SOE losses is a percentage point not needed in fresh taxes.

Cash and reserves: the PDMO is the execution engine

Papageorgiou’s emphasis on the Public Debt Management Office (PDMO) is not procedural. It is operational. Even with a strong primary balance, poor execution—wrong tenor mix, bunching of maturities, weak domestic market development—can push rollover risk back up.

Priorities:

- Publish and stick to a quarterly issuance calendar.

- Lengthen average time to maturity while keeping costs acceptable.

- Build predictable instruments for domestic investors, including long bonds and inflation-linked paper if warranted.

- Maintain cash buffers to avoid forced issuance into weak markets.

On the external side, the net international reserve floor remains on track, helped by tourism, remittances, and exports offsetting higher imports. That buffer buys time, but it must be preserved through disciplined FX operations and a credible rate regime.

Growth: the third leg of the stool

Debt ratios fall faster when growth rises above effective interest costs. The 2026 Budget can support this by:

- Prioritising permits and regulatory pruning that cut project cycle times.

- Keeping a predictable tax regime to lower risk premiums.

- Protecting trade logistics reforms that speed customs and reduce non-tariff costs.

- Ring-fencing education and skills spend that raises medium-term productivity.

Do not confuse stimulus with pro-growth composition. The former widens the deficit; the latter improves multipliers inside an unchanged envelope.

Risk map for 2026

Revenue shortfall risk. If vehicle-related taxes normalise faster than expected and core compliance lags, the primary balance is exposed. Pre-empt with conservative baselines and in-year contingency measures.

SOE slippage. Without hard constraints, arrears can resurface. Enforce cash discipline monthly, not annually.

Interest bill sensitivity. A global rate cut cycle would help. If delayed, keep domestic terming-out gradual to avoid locking in high coupons.

External shocks. Tourism is still concentration-prone. Monitor regional demand and diversify source markets to steady inflows.

What success looks like by end-2026

- A primary surplus ≥2.3% of GDP achieved on a conservative, diversified revenue base.

- Finalised restructuring agreements with remaining official and commercial creditors, executed cleanly and on schedule.

- A functioning PDMO with longer average maturities and a credible issuance calendar.

- SOE losses materially lower, with audited, published KPIs and no arrears loops.

- Reserves at or above programme floors, alongside a stable inflation path and anchored expectations.

Hit these marks and the conversation shifts—from avoiding relapse to restoring investment-grade habits over the medium term.

A practical checklist for the 2026 Budget

For policymakers and observers, this is the short list to test credibility:

Baseline realism: Are auto-related receipts booked conservatively? Are sensitivity tables published?

Compliance agenda: What concrete steps strengthen filing, e-invoicing, risk-based audits, and dispute resolution timelines?

Rule-based pricing: Are fuel and power formulas intact and used?

SOE timetable: Are transactions and performance contracts dated and measurable?

Capex quality: Is the capital budget tied to shovel-ready, growth-linked projects with procurement clarity?

Cash plan: Does the PDMO release issuance calendars and report on execution quarterly?

Social protection: Are benefits targeted, digitised, and monitored for leakage?

Conclusion: lock in the gains

Sri Lanka’s debt stock has been made lighter and its near-term profile safer. The final bilateral and commercial steps should complete a difficult restructuring chapter. The next chapter is more technical and less dramatic: steady primary surpluses, cleaner SOE finances, and professionalised debt management. That is how headline wins translate into lower risk premiums, cheaper capital, and jobs.

The IMF’s message is unambiguous. Fixing the stock was essential. Keeping the flow in line is what will make the fix last.