In the aftermath of the devastating cyclonic and flood disasters that struck Sri Lanka in late 2025, thousands of individuals and businesses have been left struggling to recover. Recognizing the urgent need for financial relief, the Central Bank of Sri Lanka (CBSL) issued Circular No. 04 of 2025 on December 5, 2025, directing all licensed banks to implement a comprehensive package of relief measures. These measures are designed to ease the burden on borrowers whose income or business operations have been directly affected, while ensuring that financial system stability is not compromised.

This analysis explains the relief package in detail, highlights its implications for borrowers, and explores how it fits into the broader disaster recovery framework.

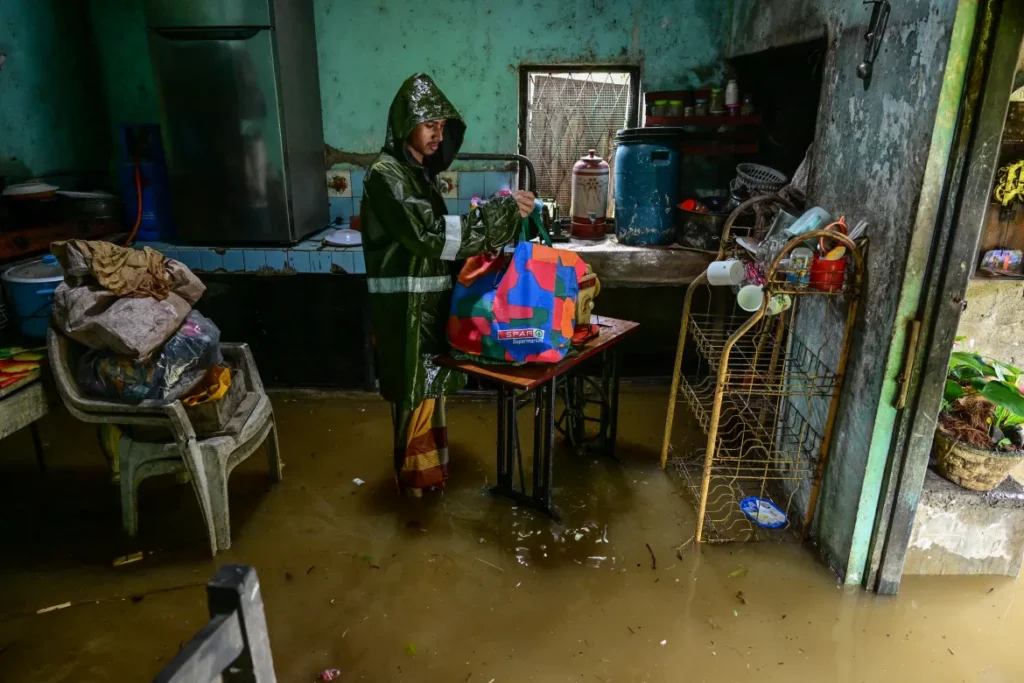

Also in Explained | Sri Lanka’s Cyclone Ditwah Recovery: The President Stressed the Importance of Stable Housing Plans

Temporary Debt Relief: Breathing Space for Borrowers

One of the most immediate challenges faced by disaster-affected households and businesses is the inability to meet loan repayments. To address this, CBSL has instructed banks to suspend repayments of capital and/or interest for 3 to 6 months on a case‑by‑case basis.

Importantly, banks are prohibited from charging interest above the contract rate during this suspension period. Furthermore, no interest will be charged on deferred interest payments, ensuring that borrowers are not penalized for circumstances beyond their control.

This measure provides critical breathing space for families rebuilding homes and businesses restoring operations after the floods and cyclones.

New Loan Facilities: Supporting Recovery and Restart

Beyond debt suspension, CBSL has directed banks to extend new loan facilities to affected borrowers. These loans are intended to provide working capital, rebuild damaged infrastructure, and restore livelihoods.

Key features include:

- Repayment begins only after a minimum grace period of 3 months beyond the suspension period.

- Loans up to 2 years will carry a maximum fixed interest rate of 9% per annum, or the borrower’s existing contract rate whichever is lower.

- For loans longer than 2 years, interest rates may be linked to the Average Weighted Prime Lending Rate (AWPR) after the initial 2‑year period.

This structure balances affordability for borrowers with sustainability for banks, ensuring that recovery financing is accessible without creating long‑term risks.

Waiver of Fees and Charges: Immediate Relief

CBSL has also instructed banks to suspend charging for cheque returns, stop payments, late payment fees, restructuring fees, and penal interest until January 31, 2026.

Where charges are automatically levied by banking systems, banks must refund them within 3 business days. This directive ensures that borrowers are not burdened by hidden costs during a period of financial vulnerability.

Transparency and Consumer Protection

To safeguard borrowers, CBSL requires banks to clearly communicate the terms and conditions of any loan restructuring or rescheduling. Borrowers must receive a full breakdown of capital, interest, and other charges before giving consent.

If relief is denied, banks must provide written reasons and inform borrowers of their right to appeal to the Director, Financial Consumer Relations Department of CBSL. Additionally, banks are prohibited from rejecting new loan applications solely based on adverse records in the Credit Information Bureau (CRIB).

This emphasis on transparency and consumer rights reflects CBSL’s commitment to fair treatment during crisis recovery.

Integration with Government Disaster Relief

The banking relief package complements broader government disaster relief measures, including housing compensation, livelihood support, and welfare schemes such as Aswesuma and Mahapola scholarships. Together, these initiatives aim to normalize livelihoods and revive businesses in a timely manner.

By aligning financial sector relief with government programs, Sri Lanka is building a coordinated framework for disaster recovery.

Implications for Businesses

For businesses, especially SMEs in flood‑affected districts, the CBSL circular provides a lifeline. Debt suspension prevents defaults, while new loans at concessional rates enable firms to repair facilities, restock inventory, and retain employees.

The waiver of fees reduces transaction costs, while the grace period ensures that businesses have time to stabilize cash flows before resuming repayments.

This package is particularly significant for industries such as apparel, tourism, agriculture, and retail, which were heavily impacted by Cyclone Ditwah.

Implications for Individuals

For households, the relief measures mean temporary suspension of loan repayments, access to affordable credit, and protection from hidden charges. Families rebuilding homes or replacing lost assets can rely on concessional loans, while the suspension of penalties prevents further financial stress.

By ensuring that banks cannot exploit borrowers during this period, CBSL has reinforced trust in the financial system.

Long-Term Significance

The CBSL circular is not just a short‑term response—it sets a precedent for disaster‑responsive banking policy. By balancing relief with financial stability, it demonstrates how central banks can play a proactive role in disaster management.

It also highlights the importance of integrating financial sector measures with broader disaster resilience strategies, including infrastructure planning, housing solutions, and climate adaptation.

Conclusion

The Central Bank of Sri Lanka’s Circular No. 04 of 2025 represents a decisive intervention to support disaster‑affected borrowers. By suspending debt repayments, offering concessional loans, waiving fees, and enforcing transparency, CBSL has provided a framework that protects individuals and businesses while maintaining financial stability.

For borrowers, this package offers hope and practical support. For the financial system, it demonstrates resilience and adaptability. And for Sri Lanka as a whole, it underscores the importance of coordinated action between government, banks, and communities in rebuilding after disasters.

As the nation recovers from Cyclone Ditwah, these relief measures will play a crucial role in restoring livelihoods, reviving businesses, and strengthening trust in the financial system.

Also in Explained | After Cyclone Ditwah: What Sri Lanka’s Disaster Readiness Really Reveals